Apr 10, 2024

benjamin-sterling

Unless you've lived under a rock for the last 5 years, if you are a business owner and you looked for financing anytime recently, you probably got bombarded with offers from dozens of brokers pretty much begging to lend you money at a "low rate" or "the best in the market rate".

If you're like most business owners, you gave it a shot because it sounded promising at first. However, it wasn't long before you did the math and noticed that the rate they offer is actually far from being low or reasonable. It is usually 20% or 30%, and sometimes it can be as high as 50% or even 100% interest!

However, you'll be surprised, but while many business owners will immediately dismiss this idea and decline the offer, unsecured financing can actually be a great solution for a lot of businesses out there.

Well, in after reading this article, you'll know exactly which group you really belong to, without further ado:

Should you even consider taking unsecured financing?

I'll start off with the elephant in the room, the rates.

While unsecured financing usually has MAJOR pros like (and I'll dig deeper on each of those points in a second):

• No personal guarantee

• No collateral

• Dynamic payments

• No time limit

• No effects on credit

The rates are HIGH, and no one can argue on that.

However, with that said, should you still even consider taking an unsecured loan even if the price is high?

The short answer is yes, well, kind of.

At the end of the day you need to understand that those unsecured loans are actually ROI based loans.

What I mean is that numbers don't lie. If you deal with a trustable lender or a broker, they will NEVER give you capital unless it provides a big positive ROI for your business.

For example, let’s assume that you need $100K for a equipment, payroll, or a marketing campaign.

Seeing how your previous equipment purchases or marketing campaigns have generated $300K in the past, you know it’s worth it, and you know that you can’t reach that point unless you’re able to get capital.

In that case, you reach out to a trustable lender, they underwrite your financing…

And immediately approve you because of it.

Yes, for borrowing $100K you will pay at least $20K to $50K (depending on different factors),

BUT:

You just received financing under 48 hours.

The repayment is relative to your sales. meaning if things go slower the payment is lower.

You don't have time limit on the repayment or effects on credit.

And to top it all up, you didn't give any guarantee, not personal and no collaterals.

So It doesn’t matter if the loan was 30% or 40% interest, it’s more than worth it, because you just did 300% ROI.

"Okay, I get it, I have positive ROI, but why shouldn't I just take a loan from the bank? "

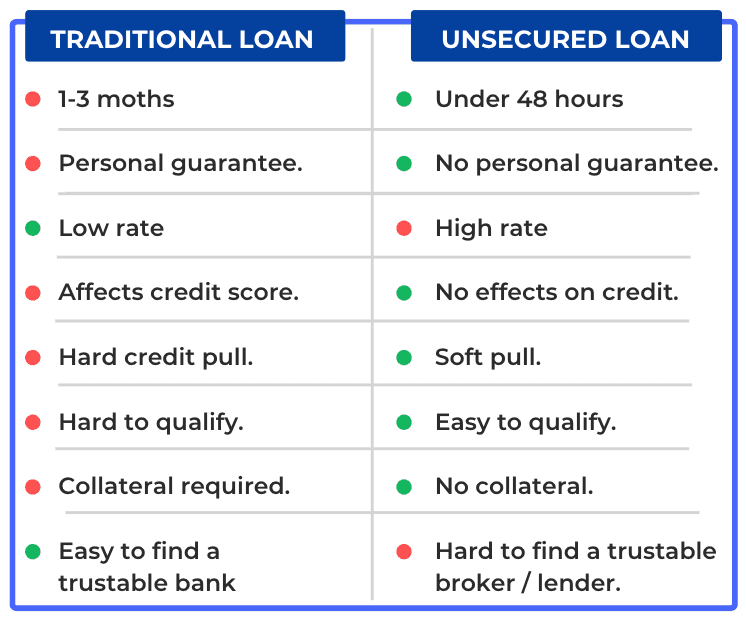

Getting a traditional loan can be a great option and cost you half or sometimes a third of what you would pay with unsecured financing.

It can be a great option especially if your credit is high, your business is very stable, you have no issue with a long process, (1-3 months), and, you can give collaterals or personal guarantee to the bank.

That's usually the case for medium-big businesses doing over $15 million a year.

But unless you can't wait couple of months now, or your credit is not high enough, or.. you simply don't want to take personal guarantee and have peace of mind - Unsecured financing will definitely be the way to go.

But that's not all, understanding that unsecured financing might be a good option for your business is the easy part. The hard part is finding the right lender borrow form. So:

How to find the right lender or broker?

It can definitely be frustrating talking to a broker or a lender and out of nowhere, get bombarded with dozens of people calling you repeatedly "just to see if you're still in the market for additional capital"..

Unfortunately, that's the case with most of the lenders/broker out there. You give out your info, and you just realized that was a huge mistake.

The reason it usually happens is because the lender/broker you're dealing with is handing out your info to dozens of other lenders get you an offer as soon as possible. Part of the lenders he is handing out your info to, are simply "selling" you as a lead to even more brokers and lenders.

Now, it doesn't mean that you don't need to go through a broker, matter of fact, it is much better to go through a broker, you just need to make sure he is reliable.

Reliable brokers usually have very good relationships with different lenders, and they will be able to get you a very good approval that you in most cases will not be able to get going out to a lender yourself (good lenders doesn't work with businesses, only with brokers).

When looking for the right broker, you want to stay away from the ones who pushing you too much or promising false promises like "we will beat any offer you got" etc.

Not to mention that if you gave out your info, and then immediately got bombarded with dozens of other brokers, you definitely want to stay away.

(Although sometimes it's inventible in the soft credit pull part, because a lot of people have access to this data and then also "sell" you as a lead to others)

Once you find a reliable broker, you'll be able to develop a good relationship with them, and next time you will need financing, they will make sure to be super flexible with you because you have a proven record of working together successfully.

Final Conclusion

There's no better way to compare traditional and unsecured loans than by outlining their differences:

Long story short, in today's world, there are more options available than ever before, sometimes too many. The good part is that numbers don't lie.

If you're a small business needing capital ranging from $20K to $5M, an unsecured loan often makes more sense. Especially if your credit is on the lower side or if time costs you more money.

P.S., I've seen hundreds of businesses who could easily take a loan from the bank, but only the waiting time needed, usually at least a month or two, ended up costing them 10x more than simply paying another 15% and get the money in the same day.

So just keep this in mind.

If more capital can boost your business, make sure to find a trustable lender that will work for you for the long term. But more importantly, DO THE MATH. If you need $40K to hire 2 more sales reps, and each sales rep generates you $30K a month, it means that waiting 2 months for a bank loan will cost you $120K.

Are you willing to take that loss? Or pay 20% higher interest (in that case $8K), and get the money tomorrow? The answer is clear.

As always, I hope it helps. Feel free to reach out if you feel that we might be able to help your business.

Golden tip - when looking for a lender/broker, make sure they offer a variety of different solutions (Line of credit / SBA / term loan/ equipment, etc). That way, (assuming they are trustworthy) they will present you all the solutions you qualify for, and who knows, maybe you'll end up paying the same rate as a loan from the bank, while taking advantage of all the other benefits unsecured financing offers.

-Ben

benjamin@savingsnyc.com

*DISCLAIMER: New York Savings serves as a trusted guide on your journey towards business financing.

Our platform is designed to offer invaluable insights, expert advice, and connects you with a range of potential lending options tailored to your unique business needs.

However, while we strive to provide accurate and up-to-date information, we cannot guarantee the completeness or accuracy of this information due to the dynamic nature of the financial industry.

Therefore, we strongly encourage all our users to conduct their own due diligence and seek independent financial or legal advice before making any financial decisions or commitments. By using our website and our services, you agree to our terms of service and acknowledge that any decisions based on information found on our site are your own responsibility.

Your engagement with New York Savings signifies your understanding and acceptance of these terms.

© New York Savings LLC. 2024